India has achieved something remarkable: 847 million citizens transact digitally via UPI. Yet step into credit and the story fractures. A business owner seeking a working capital loan navigates 7.3 separate touchpoints over seven days — with a 42 per cent chance of abandoning the process. A farmer with years of digital payment history remains ‘thin file’, paying informal moneylenders 36 to 120 per cent annual interest because formal institutions cannot see his creditworthiness.

The diagnosis is clear: severe ecosystem fragmentation. Fourteen average data sources exist per credit customer, yet only 23 per cent inform underwriting. USD 251 billion in credit demand goes unmet. Customer acquisition costs run 68 per cent higher than necessary. This is not merely a business failure — it is a social one. India processed 412 million digital transactions in a single day. Yet 52 per cent of its adult population is thin-file or no-file. That is not a data problem. It is a platform problem.

The Platform Fix: Architecture over incrementalism

The solution is not incremental system upgrades. It is a structural reimagination of how credit is originated, underwritten and delivered — through interconnected platform ecosystems where credit follows the customer. Four foundational layers drive this: an Open Infrastructure Layer for sub-500ms inter-platform communication; a Data Intelligence Layer ingesting 2.7 billion daily events; a Product Orchestration Layer spanning 14 product categories; and an Experience Layer that collapses 7.3 application touchpoints into 2.1.

Eight major platform categories — payments, lending, insurance, wealth, e-commerce, telecom, healthcare and government services — interconnect through standardised protocols, each retaining sovereignty while participating in a shared credit fabric. A telecom platform with 687 million subscribers can already offer instant credit via Account Aggregator data, with decisioning in 14 seconds and disbursement in 127 seconds. This is not theoretical. It is happening.

Big Data meets credit decisioning

Today’s underwriting models analyse 47 attributes per applicant. By 2035, platform ecosystems will process 847 — drawing on transaction histories, telecom behaviour, ecommerce patterns and geospatial signals. The result: prediction accuracy rises from 76.4 to 94.7 per cent, false positives fall by 83 per cent, and fewer good borrowers are wrongly rejected. Human intervention drops from 87 per cent of applications to just 8 per cent, reserved for the cases where it genuinely adds value. This intelligence infrastructure is built on privacy-by-design principles. The Account Aggregator framework ensures 96 per cent of data access occurs with explicit customer consent. Data minimisation protocols reduce unnecessary collection by 67 per cent. The platform economy of credit must earn trust, not merely process data.

Credit products reimagined: 2026 vs 2035

Embedded Credit: Finance that finds you

The platform era moves credit from a destination to an ambient layer in everyday life — surfacing precisely when and where it is needed. The use cases are transformative: 342 million e-commerce users accessing instant checkout credit; 94 million patients receiving treatment finance within consultation timeframes; 128 million farmers obtaining crop loans via agritech ecosystems using satellite and IoT data. By 2035, 89 per cent of credit will originate through embedded channels, up from 23 per cent today.

The USD 825 annual dividend per customer

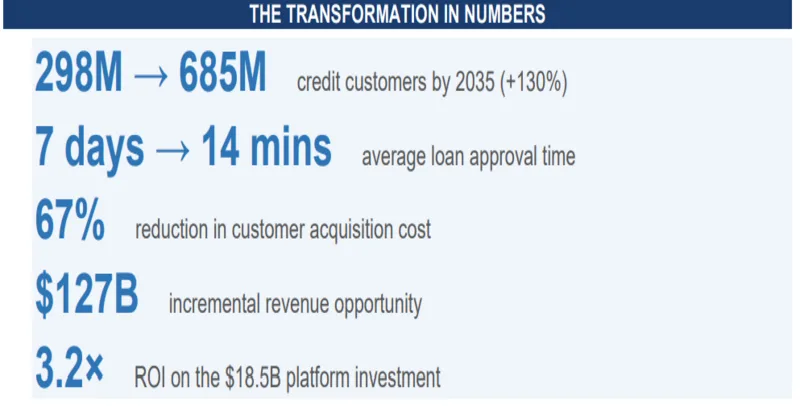

Platform integration delivers USD 825 in average annual benefit per credit customer — aggregating to USD 565 billion across 685 million users by 2035, equivalent to 1.8 per cent of GDP. Interest rates on average loans fall by 182 basis points; processing fees drop 83 per cent; application attempts halve. For the 387 million previously unserved, the gain is more fundamental: a 43 per cent reduction in informal moneylender dependence and an average USD 1,847 annual income increase through entrepreneurship.

Three phases to 2035

Phase 1 — Foundation (2026–28): Deploy Account Aggregator to 500 million users, establish API standards, launch initial ML models. Investment: USD 5.7B. Outcome: 40% automation, 180M users. Phase 2 — Scale (2028–31): Expand to 12 ecosystems, achieve 70% automation, launch real-time underwriting. Investment: USD 7.8B. Outcome: 450M users, 2.5× revenue growth. Phase 3 — Optimise (2031–35): 96% automation, full AI- driven operations, 685M users. Investment: USD 5.0B. Outcome: 3.2× cumulative ROI and sector leadership.

For CXO leadership, five immediate priorities over the next 12 months define the starting position: defining ecosystem partnership strategies, deploying a data lakehouse with Account Aggregator integration, building credit scoring and fraud detection models, launching 2–3 embedded finance pilots, and engaging actively with the RBI regulatory sandbox.

A civilisational moment

The business case is compelling — USD 127 billion in incremental revenue, 3.2× ROI, 54 per cent lower operational cost per loan. But the larger significance is civilisational. India is the only large economy to have built world-class payments infrastructure before the majority of its population had formal credit. The data, consent architecture, regulatory framework and entrepreneurial ecosystem are all in place. What remains is the decision to use them — to close the distance between 847 million digitally active Indians and 387 million still navigating credit through informal channels at ruinous cost. The decade ahead belongs to those who build that bridge.