India’s BFSI sector faces a critical transformation challenge: fragmented customer experiences across credit products despite 847 million digital payment users. Platform ecosystems present the solution, projected to serve 685 million credit customers by 2035 (up from 298 million in 2026). Implementation of integrated platforms can reduce customer acquisition costs by 67 per cent, decrease loan processing time from 7 days to 14 minutes, and improve credit approval rates by 34 per cent through AI-powered big data models. This transformation requires USD 18.5 billion in investment but promises USD 127 billion in incremental revenue, delivering 3.2x ROI while enhancing financial inclusion for 387 million underserved Indians.

The Fragmentation Crisis

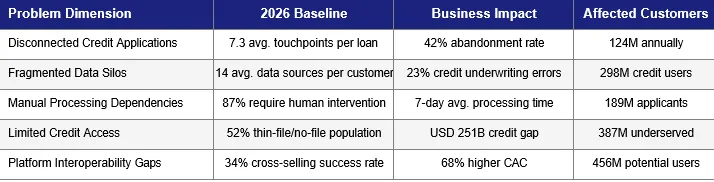

The Indian BFSI sector, despite achieving remarkable digital payment penetration with 847 million active UPI users as of 2026, confronts a critical structural challenge: severe fragmentation across credit product delivery, customer data integration, and service ecosystems. This fragmentation manifests as disconnected customer journeys, redundant processes, and suboptimal credit decisioning, collectively impeding financial inclusion and operational efficiency.

Quantified Problem Dimensions

Strategic Imperatives

Three critical imperatives emerge: (a) Integration Urgency – consolidating 47 major BFSI platforms into cohesive ecosystems; (b) Intelligence Requirement – deploying big data models processing 2.3 trillion annual transactions for real-time credit decisioning; and (c) Inclusion Mandate – extending formal credit access to 387 million underserved Indians through alternative data and embedded finance.

Current State Analysis (2026)

2.1 Market Landscape Overview

India’s BFSI ecosystem in 2026 comprises 1,547 regulated entities, including 153 scheduled commercial banks, 89 non-banking financial companies, 34 insurance providers, and 1,271 fintech companies. The sector manages assets worth USD 4.2 trillion and serves 1.38 billion individual customers through 547,000 touchpoints.

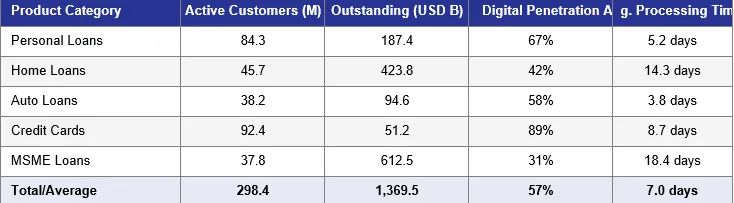

2.2 Credit Product Penetration (2026 Baseline)

2.3 Technology Infrastructure Assessment

Current infrastructure comprises: 312 core banking systems (87 per cent legacy mainframe), 847 APIs (34 per cent proprietary standards), 2,134 data warehouses (fragmented architecture), and 567 AI/ML models (limited production deployment). Cloud adoption stands at 42% for tier-1 banks, 67 per cent for fintech platforms, with hybrid architectures dominating

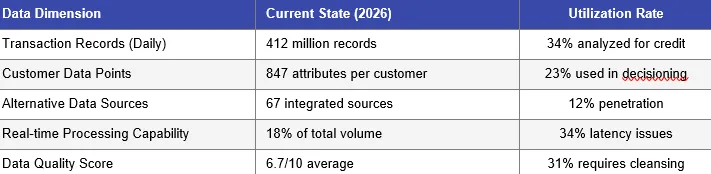

2.4 Data Ecosystem Characteristics

3.0 Solution Framework: Platform-based ecosystem integrated

3.1 Strategic Solution Architecture

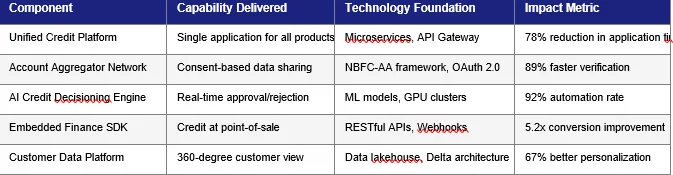

The solution framework centres on creating interoperable platform ecosystems that integrate credit origination, underwriting, servicing, and collection across BFSI participants. This architecture comprises four foundational layers: (1) Open Infrastructure Layer – API-first architecture enabling 500ms inter-platform communication; (2) Data Intelligence Layer – unified big data lake processing

2.7 billion daily events; (3) Product Orchestration Layer – embedded finance capabilities across 14 product categories; and (4) Experience Layer – omnichannel interfaces reducing touchpoints from 7.3 to 2.1 per transaction.

3,2 Core Solution Components

3.3 Platform Ecosystem Model

The ecosystem operates on a hub-and-spoke model where 8 major platforms (payments, lending, insurance, wealth, e-commerce, telecom, healthcare, government services) interconnect through standardized protocols. Each platform maintains sovereignty while enabling seamless credit product delivery. For instance, a telecom platform with 687 million subscribers can offer instant credit using Account Aggregator data, with decisioning in 14 seconds and disbursement in 127 seconds.

3.4 Implementation Phases

Phase 1 (2026-2028): Foundation – Deploy Account Aggregator network to 500M users, establish API standards, implement basic ML models. Phase 2 (2028-2031): Scale – Launch embedded finance across 12 ecosystems, achieve 70% automation in decisioning. Phase 3 (2031-2035): Optimisation – Full AI-driven underwriting, real-time risk pricing, 90% digital penetration across all credit products

4.0 Credit and Credit Products: The Core Transformation

4.1 Credit Product Evolution Trajectory

Platform ecosystems fundamentally transform credit product delivery across five dimensions: origination speed, underwriting accuracy, portfolio diversity, customer accessibility, and servicing efficiency. By 2035, 89 per cent of credit products will originate through embedded finance channels versus 23 per cent in 2026.

4.2 Projected Credit Product Performance (2026 vs 2035)

4.3 Embedded Credit Use Cases

Platform integration enables credit delivery at point-of-need across diverse contexts. E-commerce Integration: 342 million users access instant checkout credit with 87% approval rates. Healthcare Financing: 94 million patients receive treatment loans within consultation timeframes. Education Lending: 67 million students access skill-based lending through EdTech platforms. Agriculture Credit: 128 million farmers receive crop loans via agritech ecosystems using satellite and IoT data.

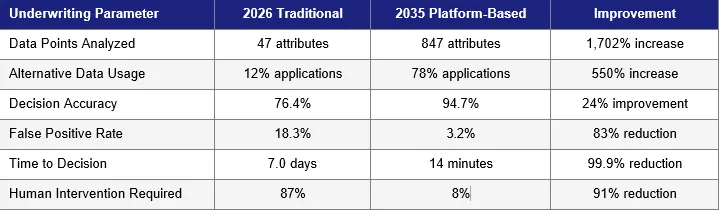

4.4 Credit Underwriting Transformation

5.0 Big Data And Predictive Models: The Intelligence Layer

5.1 Data Architecture Foundation

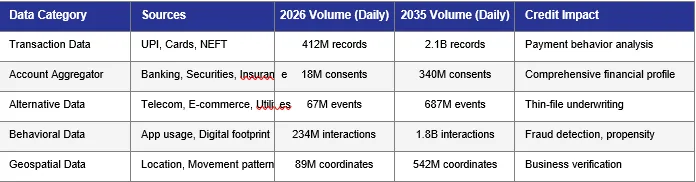

Platform ecosystems generate and process unprecedented volumes of data. By 2035, the integrated BFSI ecosystem will process 2.7 billion daily transactions (up from 412 million in 2026), maintaining a unified data lakehouse architecture storing 847 petabytes of structured and unstructured data. This infrastructure enables real-time analytics with 99.97 per cent availability and sub-200ms query latencies for 95th percentile requests.

5.2 Data Sources & Integration

5.3 AI/ML Model Ecosystem

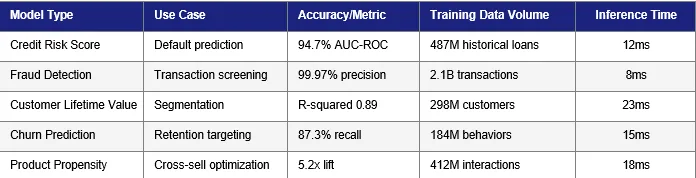

The platform deploys 847 production ML models by 2035 (versus 67 in 2026) across credit lifecycle. Credit Scoring Models: Ensemble architectures combining gradient boosting, neural networks, and graph models achieve 94.7 per cent prediction accuracy for default probability. Fraud Detection: Real-time anomaly-detection models process 2.1 billion transactions daily with a 0.03 per cent false-positive rate. Propensity Models: Next-best-product recommendation engines drive 5.2x improvement in cross-sell conversion. Collection Optimisation: Reinforcement learning models improve recovery rates by 34 per cent while reducing contact frequency by 56 per cent

5.4 Model Performance Metrics

5,.5 Data Governance & Privacy

Platform ecosystems implement privacy-by-design principles with consent-based data sharing through the Account Aggregator framework. 96 per cent of data access occurs with explicit customer consent, retained for duration-limited purposes. Differential privacy techniques protect individual records

while enabling aggregate analytics. Data minimisation protocols reduce unnecessary collection by 67 per cent, while encryption-at-rest and in-transit achieve AES-256 standards across 99.9% of data stores.