In most of the countries, every year apropos to the increase in the wages of workers, operational cost, production cost and Government taxation, a small price hike will be there in the major goods and services being offered to the public by the governments and private bodies. This is a normal phenomenon and not inflation. On the other hand, global inflation is merely a swift price rise episode in the goods and services consumed by the public due to an increase in demand and drop in supply for a certain period of time.

However, what the world is going over right now is a “Global Hyperinflation.” This is a combination of Cost Push and demand pull inflation which is an abnormal inflation. It is nothing but a peculiar whirlwind price rise in most of the goods and services consumed by the people globally for a certain period of time. This type of hyperinflation will bite every country’s primary currency that will eventually end up landing in a global recession. The current global inflation rate is approximately 8.8 per cent at the moment which is the third highest inflation rate in the last 30 years. The first and second global inflation rate was approximately 10.3 per cent and 8.9 per cent in the years 1994 and 2008 respectively. root cause of Global inflation

The current global inflation started in early 2020 and has reached its peak right now. While many have given different reasons for the cause of this weird global economic inflation and recession, the months-long curfew in most countries during the covid-19 pandemic at the beginning of 2020 led to the halt of production of goods and services and disruption in supply chain between the countries. This was followed by the change of regime and economic policies in the US, and then the Russia-Ukraine war.

The global economy was hit hard by the mandatory curfews imposed by countries because people were confined to their homes and many industries (except few service industries) halted their production and distribution altogether due to the lack of workers (man power) and raw materials. Due to which the supply-chain interrupted globally, so the economy started to move downwards in all countries. The US economy plays a vital role in the world economy for the past 4 decades. A surge or slump in the US economy and its monetary policies will always have effects for the rest of the countries in the world. On the other hand, since 2022 February, the relentless and round the clock war between Russia and Ukraine has stimulated the supply shortage of energy and food products being exported from Russia and Ukraine to other countries.

Indian Scenario

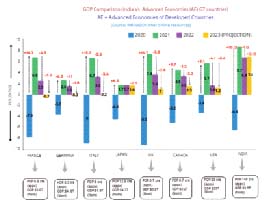

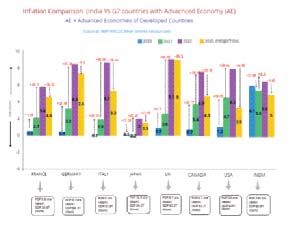

Most of the countries had faced major crisis in the supply chain of goods and services during the COVID-19 period. Consequently, economies of the world countries started shrinking and after that the outbreak of Russia-Ukraine war in early 2022 had led to the global energy crisis. This has eventually pushed the world economy towards global inflation but India’s inflation and economic growth is far better than other developed countries with advanced economies and developing countries with emerging market and economies. World has appreciated India’s sustained growth in its economy and its contribution to the world communities even after being hit hard by COVID-19. India was one of the highly populated countries which did show 8.9 per cent of GDP growth rate in the year 2021 with a massive annual change rate of 15.4 per cent from the previous year (2020). None of the world countries had recorded double digit annual growth rate except India. If we happen to consider India’s inflation rate and economic growth over the past 3 decades, India has witnessed tremendous and sustained growth since 2015.

Global comparison

Below are the comparison charts showing India’s economic growth (GDP) and inflation against advanced economies (G7 countries) and some of the emerging market economies (Developing countries). Besides my own prediction for 2023 based out of Consumer Pricing Index (CPI) and Wholesale pricing index (WPI), rest of the data given in the charts below were taken from IMF/WEO/Other online resources and follows January-December calendar year model.

Multiple Measures

Ever since this Government led by Shri Narendra Modi assumed office it has taken various price control, monetary and fiscal measures to keep the prices and inflation under control and to grow the economy. Given here some of the major control measures that are effectively being implemented till date by the Central Government in the last 8 years to enhance the GDP (Data source: National Portal of India, RBI, Indian Finance Ministry website and other online resources).

Monetary measures

Prior to COVID-19, considering the evolving global economic environment and to boost up India’s economic growth for a long-run competing with growing economies and advanced economies for a long-run also in order to get rid of the price rise problems in the retail market which sways livelihood of the middle and lower class people the Reserve Bank of India (RBI) Act, 1934 was amended by the Central Government on May 2016 so as to give statutory basis for the flexible inflation targeting framework (FITF) and it also constituted a Monetary Policy Committee (MPC) on September 29, 2016.

Current Global inflation rate is approximately 8.8 per cent at the moment which is the third highest inflation rate in the last 30 yrs. The first and second global inflation rate was approximately 10.3 per cent and 8.9 per cent in the years 1994 and 2008 respectively

The objective of this strategy was for the Central Government to fix the inflation target in discussion with RBI based out of CPI (Consumer Price Index) for every 5 years and declare it in the Gazette for public access. Some of the major objectives of this FITF are, Forecasting and targeting the inflation rate for every 5 years, retaining the fixed inflation rate with an upper and lower tolerance band for 5 years, maintaining the price stability in retail market, reducing uncertainty in the share market, boosting the GDP Growth rate and a lot more. MPC would advise RBI in setting up the repo rate for controlling inflation rate within the target. The first 5 years inflation target for the period between August 5, 2016 and March 31, 2021 was set for 4 per cent with the upper tolerance limit of 6 per cent and the lower tolerance limit of 2 per cent by Central Government on August 5, 2016 and the same was declared in the Gazette. On March 31, 2021, the central Government retained the same inflation target and the tolerance band for the next 5 year period starting from April 1, 2021 till March 31, 2026.

This is the best Monetary policy strategy ever made by RBI to control the inflation rate since independence and this well defined strategy was engineered by the then Government led by Prime Minister, Narendra Modi in 2015 and that has saved us today from this global economic downturn. Also RBI, as part of its control Measures to achieve the inflation target set forth and to promote economic growth, revises the interest rates from time to time. On December 7, 2022, RBI has revised the following interest rates, CRR: 4.50 per cent SLR: 18.00 per cent, Repo Rate: 6.25 per cent, Reverse Repo Rate: 3.35 per cent Bank Rate 6.50 per cent Marginal Standing Facility Rate: 6.50 per cent and Standing Deposit Facility rate: 6.00 per cent.

Fiscal measures

Since 2014, with the effective implementation of fiscal policy measures till date, India has been maintaining its fiscal deficit margin of around 4 per cent of total GDP but in the FY 2020-2021 the deficit went up to 9.5 per cent due to the impact of COVID-19 and the government had to increase the current expenditures to Compensate and protect the people from this Covid-19 disaster but in the FY 2021-2022 the deficit did shrink to 6.7 per cent of the total GDP which is 0.2 per cent lower than the projected deficit rate by the Finance Ministry itself due to the higher tax receipts and thrifty current expenditures as part of the decisions taken by the Central Government wisely on Monetary and fiscal policies.

For the FY 2022-2023, despite the fact that total expenditure will remain around 4.9 per cent and of which the capital expenditures will remain between 2.8 per cent and 2.9 per cent The central Government has targeted the actual GDP growth rate between 7.1 per cent and 7.8 per cent with the deficit of 6.5 per cent of the total GDP and has also planned to lower the deficit further to 4.5 per cent by FY 2025-2026. On December 6th, 2022, the World Bank upgraded GDP growth forecast for India to 6.9 per cent for FY 2022-23 from 6.5 per cent that it was projected In October 2022 stating that the Indian economy was showing higher resilience to Global Shocks and has shown extraordinary output numbers in the second quarter of FY 2022 -2023.

Price Control

- The Central Government slashed an excise duty on petrol by Rs 8 per litre and on diesel by Rs 6 per litre. The government also proclaimed that it will bear a deficit of approximately Rs 1 lakh crore an year owing to the excise duty reduction on petrol and diesel Central Finance minister Nirmala Sitharaman consistently insisted that all states should implement this excise tax cut as this would benefit the people.

- The Central Government slashed the import duty on coal from 2.5 per cent to 0 per cent and waived of the import duty on essentials raw materials and intermediaries for the steel and plastic industries On the other hand hiked the export duty up to 50 per cent for few steel products, Iron ore and concentrates to surge their availability.

- The Central Government announced a subsidy of Rs 200 per gas cylinder (to a maximum of 12 cylinders an year) to the deprived class families enrolled under Pradhan Mantri Ujjwala Yojana’ (PMUY). This announcement financially helps around 9 crore beneficiaries till date.

- The Central Government exempted the Customs duty and agriculture development cess on imports of 20 lakh metric tonnes of crude soyabean and crude sunflower oil on yearly basis and this will remain in effect till 2024 March 31st.