On June 10, Prime Minister Narendra Modi surpassed Jawaharlal Nehru as India’s longest continuously serving Prime Minister. That little marker of time, and yes, it does feel like a marker, invites honest reckoning , not celebration, not condemnation, but a clear-eyed assessment of what twelve years have built and what they have not.

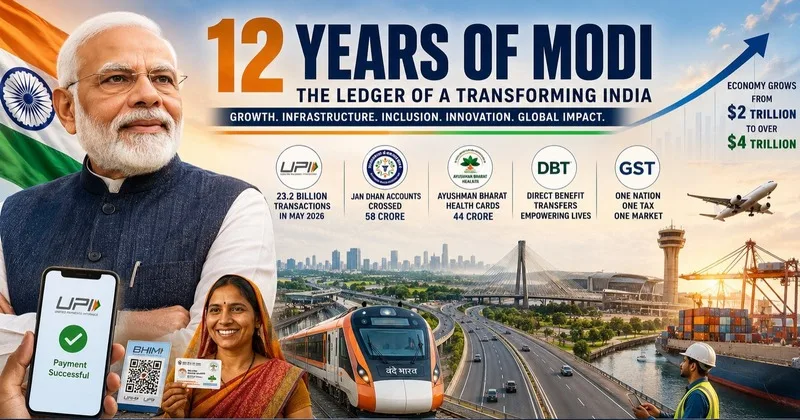

The headline number is arresting enough. India’s economy has moved from roughly two trillion dollars to over four trillion. Real GDP grew 7.7 per cent in FY26. Foreign exchange reserves stand at approximately $688 billion. By any conventional yardstick, India today is wealthier, more stable, and more consequential in global affairs than it was in May 2014. But GDP is a blunt instrument, really. The more instructive question is not how large India’s economy has become , but how fundamentally its architecture has changed. The answer, on that score, is more impressive than the headline figure suggests, and also more complicated, by a lot.

The Quiet Revolution Nobody Really Credits

The defining transformation of the Modi era isn’t a highway or a defence export milestone. It’s the construction of something far more structural: a digital-state architecture that ties identity, payments, banking, taxation, and welfare delivery together at a scale no democracy has previously tried.

Think about what this system encompasses. Jan Dhan accounts have crossed 58 crore. Ayushman Bharat has issued approximately 44 crore health cards. Direct benefit transfers move subsidies electronically, cutting the leakages that once drained welfare schemes dry. The GST, contested in its introduction, mismanaged initially, but ultimately consequential, created a unified national market and expanded the tax base. And threading through all of it is UPI, which in May 2026 alone processed 23.2 billion transactions worth nearly Rs 30 lakh crore.

That last number deserves to land properly. A public digital payments infrastructure, built on open architecture and interoperable by design, has quietly changed how hundreds of millions of Indians do daily commerce, from roadside vendors in Varanasi to exporters in Surat. Many economists now put UPI next to the Green Revolution and the telecom liberalisation of the 1990s, like a real structural turning point in India’s economic story. That is not hyperbole. It is a serious claim about how economic activity itself has changed.

This formalisation of the economy, the shift of transactions, employment, and welfare delivery from shadow to visible, is arguably India’s largest governance reform since 1991. It has improved tax buoyancy, enhanced policy targeting, and created a globally studied model of digital public infrastructure. Singapore, France, and the UAE now accept UPI. India did not merely build a payments system; it built exportable sovereign infrastructure.

Infrastructure as Industrial Policy

The second defining feature of the Modi years is basically the deliberate lift of capital expenditure into the role of the main growth motor. Public capex has climbed from something like Rs 2 lakh crore in FY15 to a budgeted Rs 12.2 lakh crore for FY27. Highways, railways, ports, airports, and freight corridors have been kept under sustained focus that, honestly, no earlier Indian government sustained over a similar stretch.

The strategic logic is close to the East Asian blueprint: smoother logistics bring down input costs, which then improve manufacturing competitiveness, and that pulls in private investment. The National Highways Authority has been building at a cadence that used to feel impossible, in Indian governance at least. Broad-gauge railway electrification has now crossed 99 per cent. One hundred and sixty-four Vande Bharat services are now operational.

Whether this infrastructure investment will generate the industrial employment India needs remains the central unresolved question. The government has bet heavily that it will. The verdict is still being written.

The Manufacturing Puzzle

Here, the assessment has to be honest about failure, or, at the very least, stubbornly unfinished. Make in India kicked off in 2014 with a clearly stated aim: lift manufacturing’s share of GDP to 25 per cent. Twelve years on, the number is still stuck between 13 and 17 per cent, depending on the way you measure it, pretty much around where it was a decade ago. That looks bad when you put it beside China at 25 per cent, Vietnam at 24 per cent, and Malaysia at 23 per cent. For an economy trying to take in a workforce growing by millions each year, this is not some minor aside. It is the unfinished centrepiece.

The Production Linked Incentive schemes have produced genuine successes in specific sectors, electronics most visibly. Here, the assessment has to be honest about failure, or, at the very least, stubbornly unfinished.

Make in India really kicked off back in 2014 with an evidently clear stated aim to lift manufacturing’s share of GDP up to 25 per cent. Now, twelve years on, the figure is still stuck around 13 to 17 per cent, depending on how you measure it , and overall it sits about where it was a decade ago. It doesn’t look great once you set it next to China at 25 per cent, Vietnam at 24 per cent, and Malaysia at 23 per cent. For an economy trying to take in a workforce growing by millions each year, this is not some minor aside. The government has responded by announcing a National Manufacturing Mission in the FY26 Budget and extending its horizon to 2035. The acknowledgement of delay is, at minimum, honest.

Employment: The Number That Never Satisfies

Employment data is where political argument and statistical methodology diverge most sharply, and where the gap between macro success and lived experience is most acutely felt.

Headline unemployment under the Usual Status measure stands at 3.1 per cent. EPFO added over 7 crore net members between 2017 and 2024. Formalisation metrics point upward. Yet youth unemployment under the more demanding Current Weekly Status measure sits around 14.3 per cent for the 15-29 cohort. And behind every unemployment statistic lies the harder question: India’s workforce grows by millions each year. Are enough productive, formal-sector jobs being created to match that demographic pressure?

The honest answer is: not consistently, not at the required pace, and not in the sectors, manufacturing, especially, where durable industrial employment is generated. This is not a partisan critique. It is the arithmetic of demography meeting the limits of a services-and-consumption growth model that has not yet made the transition to broad manufacturing employment.

A Foundation, Not a Ceiling

Twelve years on, the Modi economic record is one of genuine transformation in some dimensions and genuine incompletion in others. The digital-state architecture is a historic achievement. Infrastructure investment is real and compounding. Financial inclusion has changed what ordinary Indians can access. Banking sector repair, often underappreciated, removed a brake on investment that had been binding since the NPA crisis of the early 2010s.

Still, per capita income growth, the degree of manufacturing depth, plus the steady creation of high-quality jobs, remain as the economy’s most unresolved imperatives, no joke. India’s people are now comparing their own outcomes to China’s path, to Southeast Asia’s manufacturing upturn, and to Gulf prosperity too, not really to what India used to be. That shifting reference point is, in its own way, a consequence of the ambition this era has generated.

If the next decade delivers on manufacturing and employment what the last twelve delivered on digital infrastructure, the Modi era may well be remembered as the foundation phase of India’s emergence as a genuine great power. If it does not, the distance between India’s potential and its performance will remain the central story of its economics and its politics. The ledger is open. The accounting continues.