The functioning of the public sector banks has been shoddy all along. The Congress made no sincere efforts to streamline it. The onus is on the Modi Government to usher in reforms in a big way

The functioning of the public sector banks has been shoddy all along. The Congress made no sincere efforts to streamline it. The onus is on the Modi Government to usher in reforms in a big way

Dr Sunil Gupta

The Public Sector Units (PSUs) were famously declared as ‘temples of modern India’ by the first Prime Minister, Jawaharlal Nehru. Nehru was a follower of the Soviet model of growth, which can be understood as one that is led by state-sponsored enterprises rather than privately-owned companies. Nehru and his cabinet ushered in an era where the state ownership and control over most large companies was a norm and the rationale given behind this move was that in such a state of affairs development will be equitable and resources and income will be distributed among all citizens without disparity.

Cut to 2018. We come across a scam where a diamond merchant could dupe country’s second largest public sector bank in connivance with officials and stay undetected for more than 7 years. But the point here is, should we discuss this case in isolation or shall we carefully take into consideration all that has been happening since we gained Independence?

For some time forget Bofors, 2G, Coalgate and other scandals that cost the government and public lakhs of crores of money. The UNICEF report released today ranked India 12th worst nation among low-income countries with respect to infant mortality rate; in the year 2016, 6 lakh infants died in their first month. Same is the condition when we talk about access to clean drinking water, education and healthcare. The question is ‘Why do we fare so poorly on almost every socio-economic indicator?

The reason is that money and resources that belong to the downtrodden have, for most of the years in post-independence India, been swallowed by the rich and the government either acts in connivance or fails to bring the conspirators to justice. In scams such as 2G, Coalgate and Bofors, government ministers and bureaucrats get directly involved in looting the money; in cases where businessmen acquire loans through unfair means never to be returned to lending institutions, the government plays a role from behind the curtain.

How the scam workedIt is a general business practice of underwriting loans in the banking sector. Banks issue Letters of Undertaking (LoU) whereby they guarantee to other banks, which subsequently give loans, that if the importer (who needs credit for importing raw goods and promises to pay once he earns revenue through sales of finished goods in domestic or foreign market) doesn’t honour his commitment, the LoU issuing bank shall pay other banks on importer’s behalf. |

In Nirav Modi-PNB case, one must refrain from making any judgment until investigating agencies come out with a comprehensive report on how bank officials and others could inflict damage as high as third of the market value of PNB. But we can surely pray that real culprits, no matter how influential they are, are brought to justice and junior level executives are not made scapegoats.

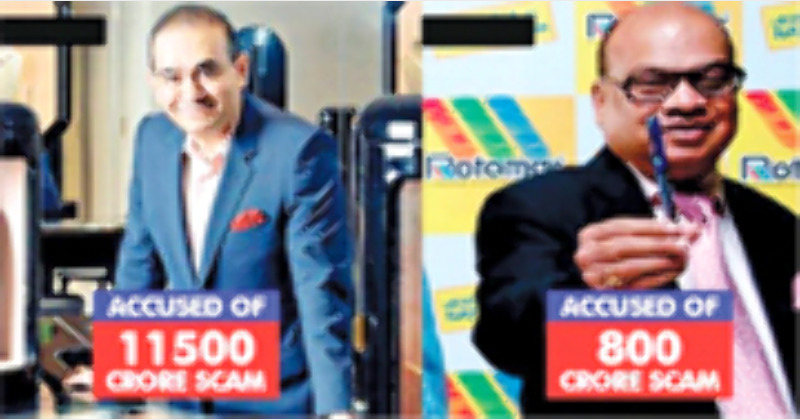

A detailed guide to how the PNB fraud came into being and could last for so long is at the end of this write-up. We should now take into consideration how our nationalized banks are being plundered. Letters of Undertakings in the Nirav Modi case were not only unauthorised with respect to the sanctioned limit but also were issued without any collateral from the importer of rough gems. The final amount of above INR 11,000 crore is an outcome of regular rollovers of LoUs since Nirav Modi firm did not have the capacity to pay back earlier amounts—akin to a Ponzi scheme. The most alarming part is that we do not know how many PSBs are similarly exposed to such risky non-fund based credit to importers, backed by nil or less than proportionate collateral.

Sadly, the rot did not stop when Nehru’s successors took over the reins of the Congress party. Next was Indira Gandhi, the daughter of a socialist father. She came up with the idea of nationalising Indian banks and did so by enacting the Bank Nationalisation Act in 1969. The Act was preceded by an Ordinance on the same matter and gave the country that the then Prime Minister promised would serve as drivers of inclusive growth, of the public sector banking institutions.

The alleged intention behind nationalising Indian banks was that the downtrodden could not hitherto access banking facilities and through state ownership, priority lending would become the overriding principle of our banks. What followed this was the wave of globalisation and exactly after two decades India too opened its doors to foreign investment, the license-era and inspector-raj came to an end with government’s stance on liberalisation.

The joyful ride, however, was short-lived. At a time when these lending institutions had to exercise extra vigilance while extending loans, especially for big-ticket projects, they failed in their job. And to exacerbate the pain, ministers and bureaucrats who could exert pressure and wield power, used their dominant positions in helping many corporates secure loans from public sector banks.

The UPA-led governments from 2004 until 2014 not only gave the country scams like 2G and Coalgate but also inflicted damages that are cropping up till date. Institutions like public sector banks and central bank of the country were so deeply under the phase of inaction that only after the shift in government could they realise how bulky and deep the issue of non-performing assets (NPAs) is and that it is a now or never option for Reserve Bank of India (RBI) to come up with corrective actions.

Also, chartered accountants’ nomination for shareholder category directorship is, in most of the cases, rejected by the election committees of PSBs on directions of the Finance Ministry. A person who has the capability to bring financial prudence to the board is thus not allowed to enter. When CAG undertakes or supervises the audit of enterprises where public money is involved, a PSB cannot be allowed to appoint its auditors on its own, a state where independence of auditors ends and they act as a mere puppet of the bank board. It is to be noted that RBI was the appointing authority of statutory auditors of PSBs till a decade back.

The Modi-led government needs to correct these flaws, to begin with.

In 2014, when policymakers changed and the Modi-led council of ministers took charge, the RBI took cognizance of some issues and reprimanded banks on giving an incorrect and doctored picture of their books where bad loans were masked so that investors and other stakeholders be kept under an impression that the entity was financially healthy and viable.

It was only when decision-making became quick and prudent after the 2014 polls that bills related to insolvency and bankruptcy, benami property and black money (undisclosed foreign income and assets) could be presented in the Parliament. It was through an ordinance that the Modi-led government gave special powers to RBI to direct lenders to invoke insolvency proceedings against willful defaulters so that the NPA mess could be sorted out before it swells into an unbearable and incurable balloon.

The way ahead for the current dispensation is to keep its reformist agenda going without bowing to the hurdles created by the opposition and some section of media with vested interests. The Nehruvian ideology where public sector undertakings developed into nothing but institutions of corruption and inefficiency can no longer be the preferred policy of the government. It is time that we accept shifts such as the new indirect tax regime, scrapping of higher currency notes and divestment of government stake in PSUs.

(The writer is a former director of a Nationalised Bank)