Goods and Services Tax (GST) stands today as one of the most transformative economic reforms of independent India. When it was first introduced in 2017, skeptics dismissed it as the so-called “Gabbar Singh Tax,” arguing that it brought additional burdens for citizens and businesses. The truth, however, was quite the opposite. The real villain lay in the fragmented pre-GST system—a confusing mesh of excise duties, service taxes, and state-level VAT that encouraged inefficiency, inflated costs, and bred rent-seeking. Trucks were forced to idle for hours at State borders, small firms struggled with multiple filings under different authorities, and consumers ultimately paid the price for this chaos. GST replaced that disjointed legacy with a single, unified framework, lowering tax rates on daily essentials and bringing about a more rational and transparent system.

Embarking on Growth Oriented Journey

Eight years on, India has embarked on the next phase of this journey with the launch of GST 2.0 in September 2025—a refinement that simplifies rates, reduces compliance burdens, and makes taxation more growth-oriented. In its original design, GST adopted a four-slab structure—5, 12, 18, and 28 per cent. That arrangement was essential at the time to secure consensus, as States were reluctant to accept the risk of losing revenues under a brand-new system. But while consensus-building was necessary, the compromise also created complexity and gave rise to frequent disputes that ran against the founding principle of simplicity. GST 2.0 is the long-awaited correction: two primary slabs of 5 and 18 per cent, along with a demerit rate of 40 per cent reserved for luxury and sin goods. This streamlined structure reflects both confidence and maturity, showcasing a system that has stabilised in terms of revenue and compliance.

Timely Tax Reforms

The timing of GST 2.0 is no less important. The global economy is passing through an era of uncertainty, with trade disruptions, tariff conflicts, and inflationary pressures weighing heavily on businesses. In this context, India’s reform delivers a timely domestic stimulus by lowering compliance costs, easing working capital strains, and cutting rates in mass-consumption and labour-intensive sectors. The outcome is not merely financial but also strategic: simpler processes reduce litigation, lighter regulations free management bandwidth, and enterprises are better placed to channel their resources into investment and expansion. When viewed alongside broader structural reforms, the redesign of GST contributes to India’s positioning as a competitive, stable production base at a time when global value chains are being reshaped.

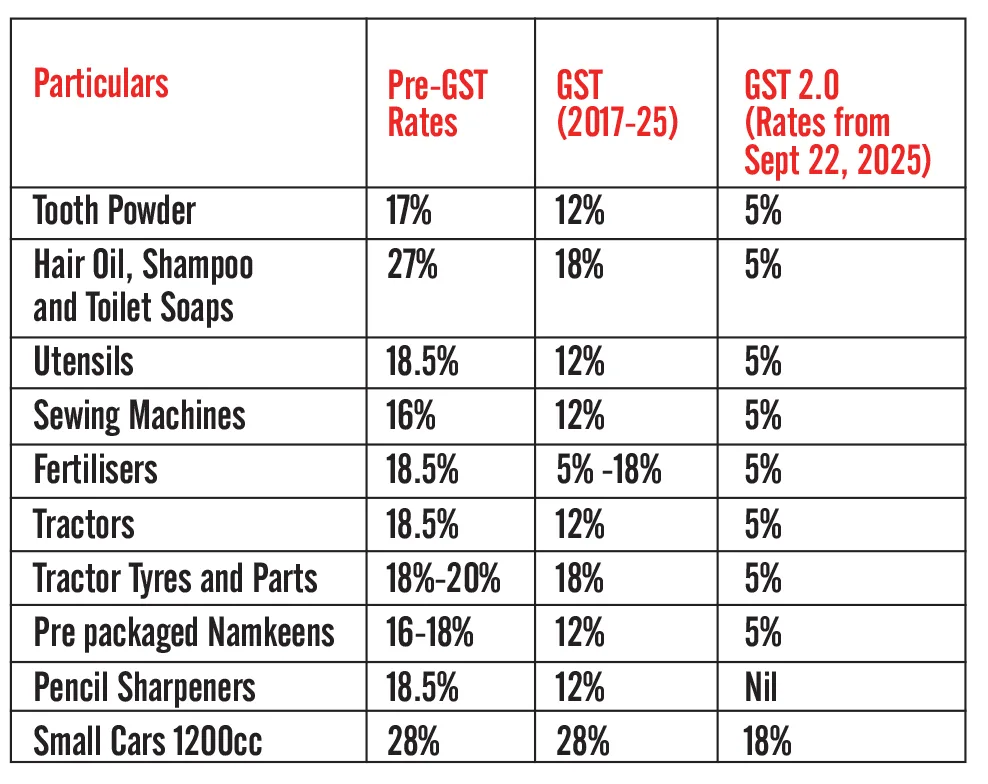

The changes introduced under GST 2.0 are substantive and visible across sectors. Everyday essentials and mass-consumption goods have shifted into the lowest slab of 5 per cent, directly benefiting households and reinforcing consumption demand. Industrial inputs have largely been placed under 18 per cent slab, reducing cost burdens for firms and creating a more rational structure for value chains. Over 33 lifesaving medicines have been exempted entirely, along with basic dietary items such as milk, paneer, and chapatis, ensuring that vulnerable households and patients experience direct relief. At the same time, important sectors like automobiles, cement, and electronics have witnessed steep tax reductions, encouraging affordability and driving growth momentum.

The rollout ahead of the festive season further maximises the impact by immediately stimulating household spending and bolstering business confidence.

The evolution of GST clearly shows how Indian households have been steadily gaining from a reduction in effective tax rates since its inception. What began as a structural reform in 2017 has now matured into GST 2.0 under the leadership of Prime Minister Narendra Modi, delivering both simplification and substantial relief to common citizens. According to SBI Research, the weighted average effective GST rate has fallen to about 9.5 per cent today, compared to 14.4 per cent when the system was first introduced. Out of 453 goods whose rates were revised under GST 2.0, an overwhelming 91 per cent witnessed tax cuts. Nearly 295 goods moved down to the 5 per cent or nil category from the earlier 12 per cent slab, a decisive turn in favour of household welfare.

Consumption-Led Momentum

The reform is also expected to inject new life into India’s consumption story. Estimates from SBI Research suggest that the GST adjustments could directly spur additional consumption worth Rs 70,000 crore, thanks to Rs 85,000 crore in tax relief and a marginal propensity to consume of 0.7. When multiplier effects are factored in, total demand is projected to rise to nearly Rs 1.98 lakh crore. The Government has pegged the net annual fiscal cost of these reductions at around Rs 48,000 crore. However, SBI anticipates that buoyancy in economic activity and a widening tax base will cap the actual revenue impact at only about Rs 3,700 crore. Crucially, when these changes are seen alongside recent income-tax reforms, the total demand boost could touch Rs 5.31 lakh crore—equivalent to around 1.6 per cent of GDP. This stimulus alone has the potential to lift India’s growth trajectory by 100–120 basis points, taking GDP growth towards 6.5 per cent in FY26 and possibly 7 per cent in FY27.

Simplification and Systemic Gains

The Modi Government has ensured that GST 2.0 goes beyond rate rationalisation. The reform also addresses structural and compliance bottlenecks, which had long troubled businesses. Automatic registration, faster refunds, and provisional input credits ease the burden on working capital, while the removal of inverted duty structures levels the playing field for disadvantaged industries. MSMEs, which are the backbone of India’s economy, have been empowered through simpler filing requirements and easier financing options via platforms like TReDS that facilitate quicker invoice discounting. On the logistics front, the core gains of ‘One Nation, One Tax’ have been deepened with greater digital integration, reducing interstate delays and enhancing supply-chain efficiency. Reform, however, is not a one-off event but a continuous journey. GST 1.0 had already replaced the complex pre-2017 regime of excise, VAT and service taxes; GST 2.0 now takes the system closer to the ideals of simplicity and fairness. Future improvements can build on this foundation, from streamlined dispute resolution through a GST Appellate Tribunal to faceless assessments, stronger ITC reconciliation, and data-driven governance through GSTN analytics. Innovative proposals such as Aadhaar-linked dynamic relief cards could also make assistance even more inclusive in the years ahead.

Charting the Next Phase

Ultimately, GST 2.0 is not just a tax reform but a milestone in India’s economic transformation under Prime Minister Modi’s vision of building an inclusive and Aatmanirbhar Bharat. By enhancing household purchasing power, rationalising rates, simplifying compliance, and giving industries room to grow, this next-generation GST strengthens consumption, investment, and overall vibrancy in the economy. In the current global climate of ˘ uncertainty, it sends a powerful signal that India is committed to stability, competitiveness, and growth powered by forward-looking reforms.n

Comments