“This India is different from what it was in 2013,” said the multi-national investment bank, Morgan Stanley, in its report titled ‘How India Has Transformed in Less than a Decade.’ The report describes how India has “gained positions in the world order with significant positive consequences for the macro and market outlook,” in the last decade, under Prime Minister Narendra Modi. As per the report, India “will emerge as a key driver for Asia and global growth.”

The report presents a snapshot of the significant changes in the past decade and their implications. The report states, “We run into significant skepticism about India, particularly with overseas investors, who say that India has not delivered its potential (despite its being the second-fastest-growing economy and among the top-performing stock markets over the past 25 years) and that equity valuations are too rich.”

“However, such a view ignores the significant changes that have taken place in India, especially since 2014. We highlight the 10 big changes, mostly because of India’s policy choices, and their implications for its economy and market,” the report added.

The report highlights 10 big changes – Supply-Side Policy Reforms, Formalisation of The Economy, Real Estate (Regulation and Development) Act, Social Transfers: Direct to Beneficiary, Insolvency and Bankruptcy Code, Flexible Inflation Targeting, Focus on FDI, India’s 401(K) Moment, Government Support for Corporate Profits and MNC Sentiment at Multiyear High – as factors contributing to India’s transformation in the last decade.

Supply-Side Policy Reforms

The report states that India’s infrastructure has picked up pace in the last eight years. Furthermore, the report provides a snapshot comparing infrastructure progress before and after 2014. The report reveals that the pace of building national highways has doubled in the past decade. The report shows that while about 25,700 km of national highway was built between 2006 and 2014; since 2015 about 53,700 km of national highway has been built.

Furthermore, the report revealed that the pace of internet penetration in India has increased multi-fold since 2014. It shows that while 58.9 million broadband subscribers were added between 2006 and 2014; since 2015 about 771.3 million broadband subscribers were added.

The report also highlights the multi-fold increase in the production of renewable energy. India added 95.7 gigawatts (GW) of renewable energy since 2016, whereas a mere 25.7 GW was added between 2006 and 2014. The report further shows that about 42.3 per cent of railway routes was electrified since 2015, whereas a mere 6.3 per cent electrification between 2006 and 2014.

Formalisation of the Economy

The investment bank has highlighted that GST collections are on an upward trend. The snapshot highlights that GST collections are at about 6.7 per cent of India’s GDP. Furthermore, the report highlights the adoption of digital payment systems in India. The snapshot shows that digital transactions now constitute, in 2023, about 76.1 per cent in comparison with India’s GDP, whereas in 2016, digital transactions were at 4.4 per cent of the GDP.

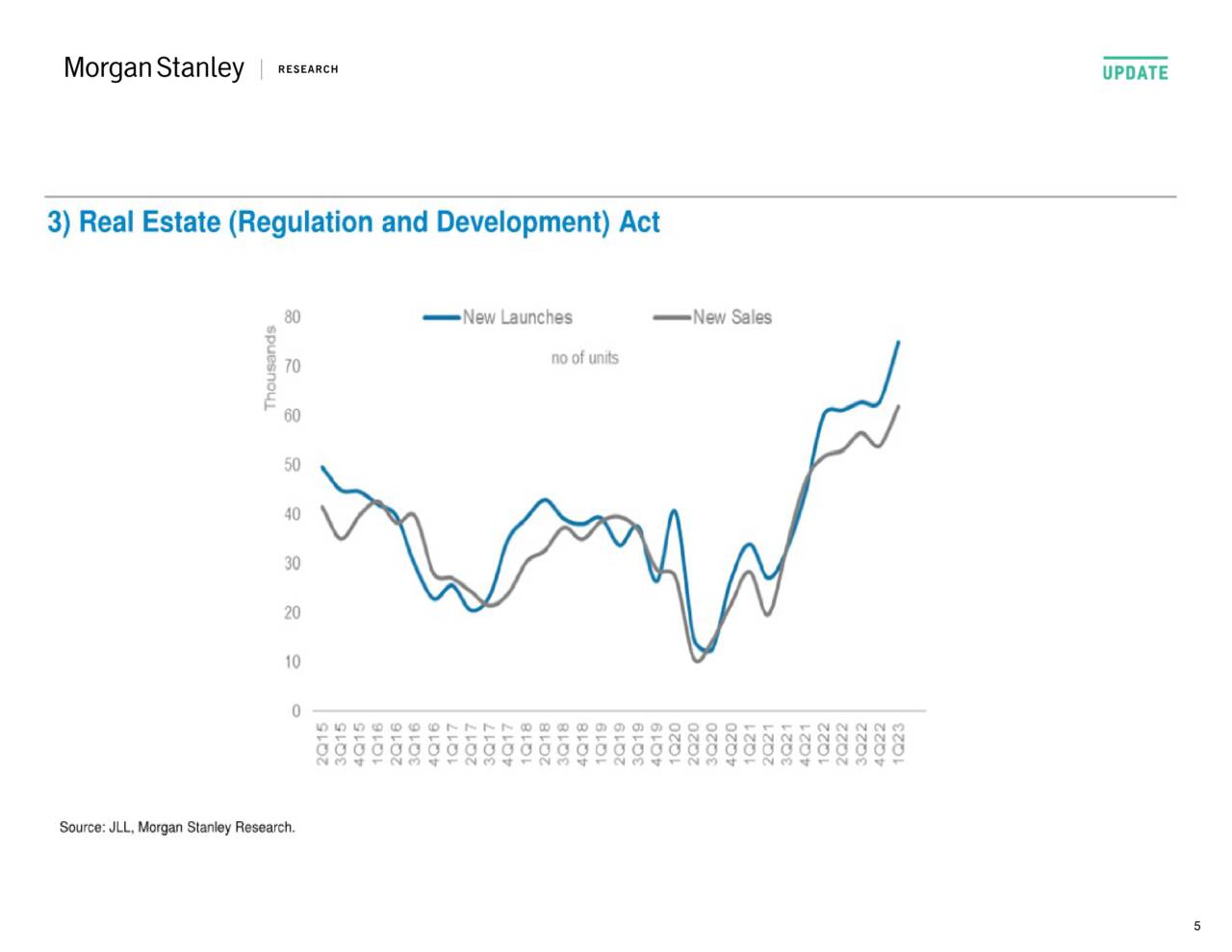

Real Estate (Regulation and Development) Act

The report provides a snapshot of new launches and sales since 2015. While the real estate market witnessed its worst period during the 2nd and 3rd quarters of 2020 i.e. during the Covid-19 pandemic, it has recovered to a new high with about 75,000 new units launched and 60,000 new units sold in the 1st quarter of 2023.

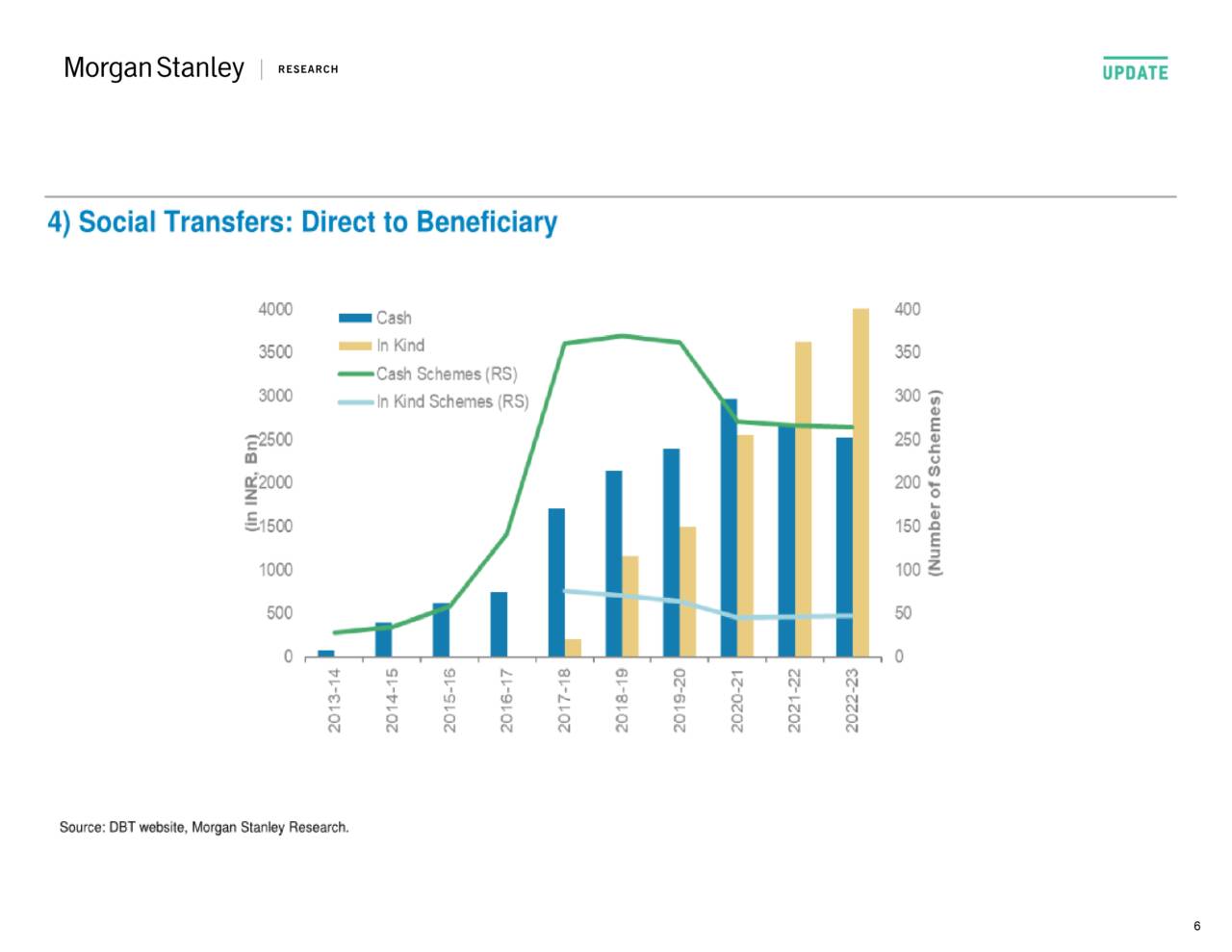

Social Transfers: Direct to Beneficiary

The report highlights the significant growth in direct-to-beneficiary schemes over the past decade, indicating a multi-fold increase compared to the 2013 data. The snapshot reveals while the number of social welfare schemes has increased, the transfer amount which grew during the height of the pandemic has now plateaued.

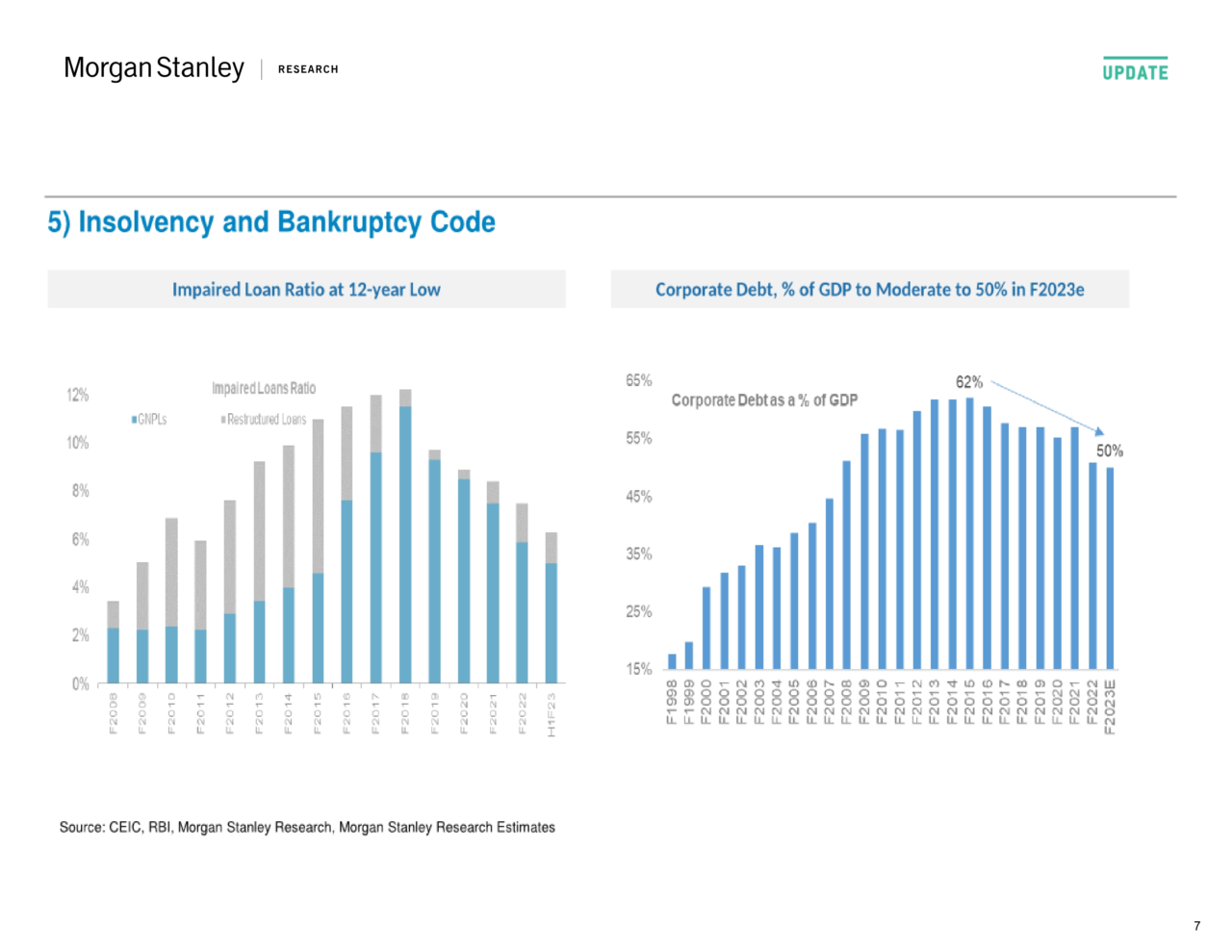

Insolvency and Bankruptcy Code

The report states that the impaired loan ratio is at a 12-year low, due to the Insolvency and Bankruptcy Code. The impaired loan ratio was at its peak during 2017-18. Furthermore, the report highlights that corporate debt, as a percentage of GDP, is expected to moderate around 50 per cent in F2023 compared to the high of 62 per cent in 2015.

Flexible Inflation Targeting

The report states that the flexible inflation targeting regime has allowed India to reduce year-on-year inflation. Furthermore, the snapshot highlights the high inflation between 2009 to 2014, stating that the high inflation was driven by loose monetary/fiscal policy. The report also highlights the decoupling of FED and RBI’s policy rate hike cycle.

Focus of FDI

The report states that India has maintained its focus on Foreign Direct Investments (FDIs), with Gross FDI reaching above USD 350 billion in 2023.

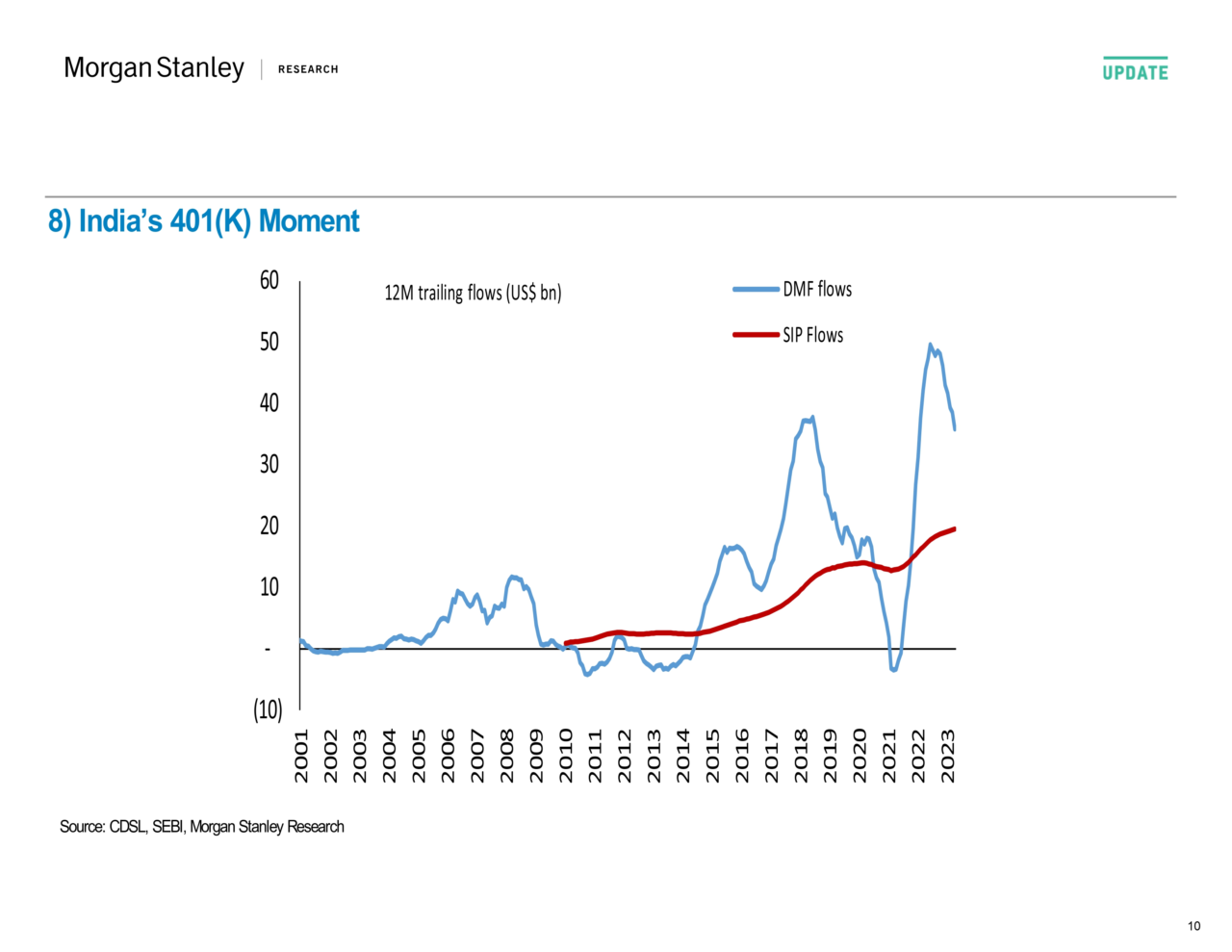

India’s 401(K) Moment

The report shows that retail participation has increased through mutual funds, with SIP inflows.

Government Support for Corporate Profits

The report shows that there is a rise in corporate profits due to the government’s support. The snapshot contains a log scale indicating the rise in nominal GDP and earnings indexed to 100, from 1994 to 2022.

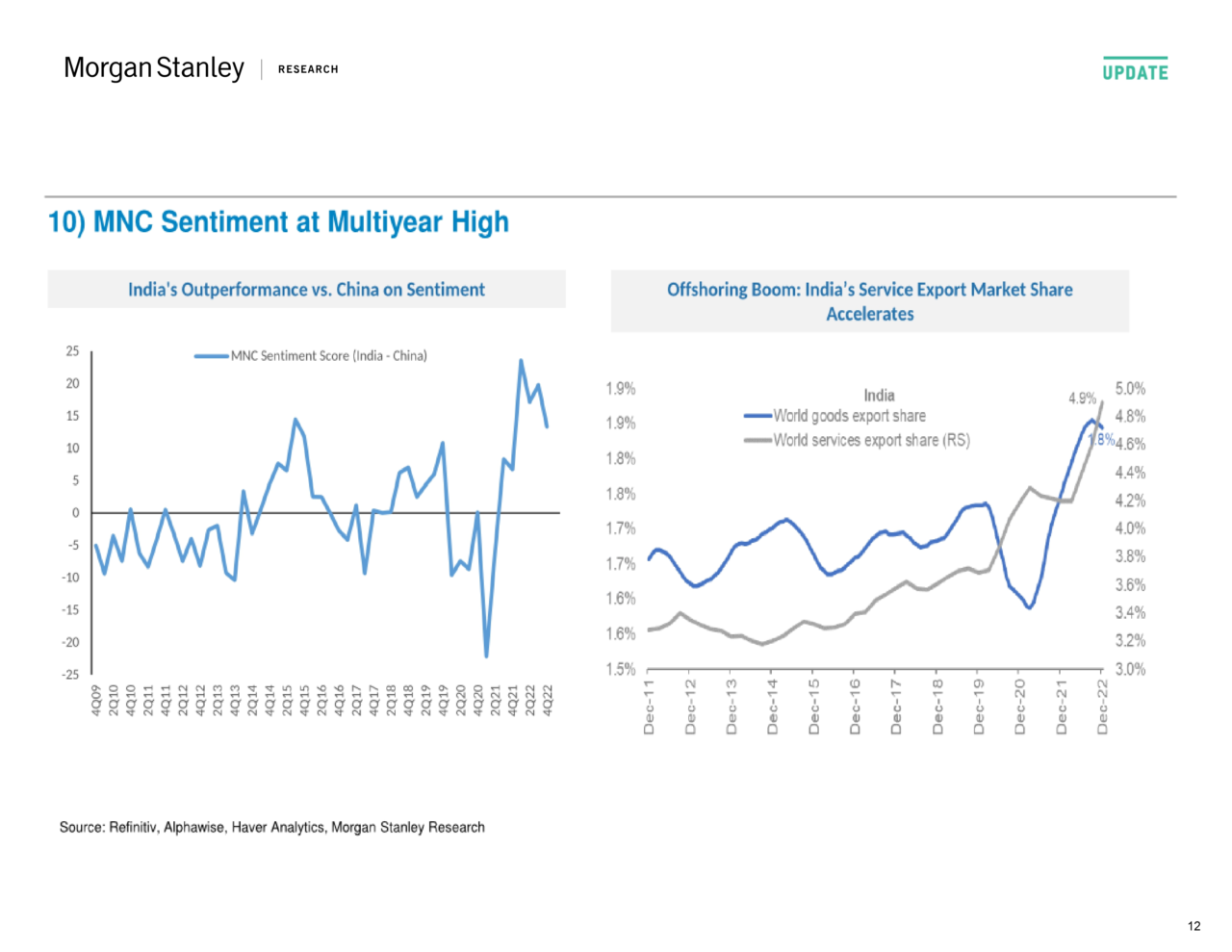

MNC Sentiment at Multiyear High

The report shows that the sentiment of multinational corporations (MNCs) is higher towards India, compared to China. Furthermore, the snapshot shows that India’s service export market share has accelerated since 2011. The report shows that India’s share in world goods export stood at 1.8 per cent and its share in world services export stood at 4.9 per cent in December 2022.

The Macroeconomic Implications

The report states that manufacturing and capital expenditure, as a percentage of the GDP, is expected to rise steadily. The investment bank said, “We expect a new cycle in manufacturing and capex, as we estimate the share of both to rise in GDP by approximately 5ppt by 2031.”

Furthermore, the report states that India’s market share in exports is expected to more than double to 4.5 per cent by 2031. “We estimate that India’s export market share will rise to 4.5% by 2031, nearly 2x from 2021 levels, with broadbased gains across goods and services exports,” Morgan Stanley said.

The report also states that a major shift in the consumption basket is expected as household income is expected to increase in the next decade. The report states that the GDP per capita is expected to increase from USD 2,278 to USD 5,242 in 2031. As per the investment bank’s report, households with income below USD 5,000 will decrease from 38 per cent in 2021 to 13 per cent in 2031. Furthermore, households with income between USD 5,000 and 10,000 will also decrease from 36 per cent in 2021 to 34 per cent in 2031.

As per the report’s forecast, households with income between USD 10,000 and 35,000 will increase from 24 per cent in 2021 to 46 per cent in 2031. The report further indicates that households with income above USD 35,000 will increase from 2 per cent in 2021 to 7 per cent in 2031.

The investment bank said, “As India’s per capita income increases from US$2,200 currently to about US$5,200 by F2032, this will have major implications for change in the consumption basket, with an impetus to discretionary consumption.”

Furthermore, the investment bank’s report indicates lower volatility in inflation moving forward and shallower interest rate cycles. The report read, “We expect inflation to remain benign and less volatile, which would imply shallower rate cycles. Shallower rate cycles could also imply more benign equity market cycles.”

The report further forecasts a positive trend in the current account deficit. The report states, “We expect a virtuous cycle of higher saving and investment, which will help CAD to narrow steadily,” between 2023 and 2033. “We believe India’s structural transformation will feed into the saving-investment dynamics, implying gains for its external balance sheet, with a progressively narrower trend in the CAD,” the investment bank said.

The Stock Market Implications

“Indian companies will likely witness a major increase in their profits share to GDP. Triggered by supply side reforms by the government, we expect a major rise in investments coupled with a moderation in the current account deficit and an increase in credit to GDP to support this rise,” said Morgan Stanley.

“The share of profits in GDP has doubled from all-time lows hit in 2020 and are set to rise further – maybe even double from here – leading to strong absolute and relative earnings. This explains India’s apparently rich headline equity valuations. Triggered by supply-side reforms by the government, we expect a major rise in investments, a moderation in the CAD and an increase in credit to GDP to support the coming profit growth,” the report read.

“Lower share of foreign portfolio (FPI) in current account funding has reduced the stock market’s negative return correlation with oil prices, especially when oil prices rise due to supply disruption,” the report added.

Furthermore, on India’s lower correlation with the US recession, the investment bank said, “As India’s reliance on global capital market flows has reduced, the market’s sensitivity to a US recession and US Fed rate changes also seems to be fading.”

“This reflects persistent domestic demand for stocks and higher growth for longer. India is trading at a premium to long-term history, albeit well off highs and in line with recent history,” read the report.

The investment bank has further highlighted certain risks – a global recession, a fragmented general election outcome in 2024, a sharp rise in commodity prices due to supply outages and shortages in skilled labour supply.