Using hoarded currency notes for illegal transactions by free riders artificially inflates prices and hurts poor and middle class. Demonetization, therefore, helped RBI to sustain a low inflation regime.

Amarendra Pratap Singh

Let us deal with it. Prime Minister Narendra Modi invoked demonetisation and history will judge whether or not he stands among most risk-loving politician in post-liberalisation India. Demonetisation will stay in the political and economic history of India and so will the PM. Since its announcement in November 2016, the jury is out to do a cost-benefit analysis and mainstream intellectuals are convinced that demonetisation was badly implemented and lacked economic logic.[1] While a few articles are available regarding its short-run effects; what we know for sure is that no objective assessment of demonetisation effects is available.[2] [3]

Government agencies have also been very conservative in providing information regarding demonetisation effects and available information is sporadic and incomplete. What we know through government sources is that tax buoyancy and personal income tax base increased in post demonetisation period.[4] While demonetisation definitely hurt economic growth in the short run, economic growth cannot be the only criterion to judge demonetisation exercise. Demonetisation was also a redistribution exercise in which beneficiaries were not selected by the state but they participated voluntarily. Every redistribution exercise brings pain and is poised to be costly in the short run, however, its medium and long-run effects on the economy shouldn’t be ignored.

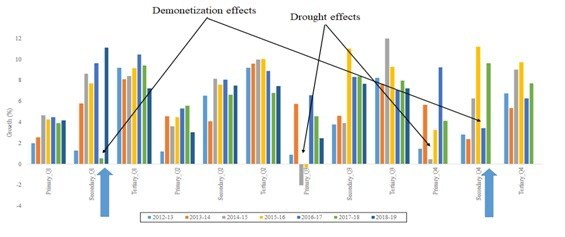

Currency note[5] [6] is a scarce resource in the sense that it is critical for expansion of bank credit and Central Bank, RBI, only can issue currency notes. Being quasi-fixed in supply, currency notes extract scarcity rent. Hoarding of currency notes hurts the formal economy and expand illegal economy which eventually hurts poor by reducing tax revenue to the government and contributes to increase inequality and public disorder. Using hoarded currency notes for illegal transactions by free riders artificially inflates prices and hurts poor and middle class. Demonetisation, therefore, helped RBI to sustain a low inflation regime. Along with demonetisation, there has been a sustained drive against illegal property. While pointing fingers towards low growth, intellectuals conveniently ignore the inflation effects of demonetisation. GDP growth (quarterly to quarterly) data shows that demonetisation had minimal effects on primary sector activities and its effects on secondary sector activities lasted for two quarters only.

Table: Sector wise quarterly GDP (constant prices) growth (2012-13 to 2018-19)

Another way to analyse demonetisation can be to evaluate demonetisation in a historical and contemporary context with other similar policy decisions. Historically, a comparable exercise to demonetisation in post-independence India was land reforms. One can judge the success of land reforms in whatever way but nobody can doubt efficiency increasing effects of land reforms to increase the investible surplus. Still, historians argue that fear of losing land induced Muslim landlords in north India to join Pakistan movement.[7][8] Despite its limited implementation success, land reform in India is regarded in good spirit and all praise goes to the then Prime Minister Jawaharlal Nehru. CPI/CPM ruled Bengal for 30 long years without any effective opposition by doing simple land reforms in an effective manner. It is only from the perspective of landlords; land reforms can be termed as an immoral act.

Another perspective to explain land redistribution is that it was a political stunt by Congress Party to grab vote of poor. In the same fashion, cash was hoarded by a handful of individuals who gained from crony capitalism during UPA I&II. Like land reform, short-run effects of demonetisation are definitely more at the negative side but not amounting to human lives. Millions died due to partition within months which was the short run cost which people paid. In terms of short-run cost, demonetisation, therefore, has been a better resource redistribution exercise than land reforms. If demonetisation was money laundering exercise, land reform was land abduction by Nehruvian Congress to win elections. Additionally, criticism of demonetisation as money laundering exercise inherently suggests that centralised redistribution generates better outcomes in comparison to market-driven redistribution of resources.

As far as success is concerned, the demonetisation story looks similar to the story of land reform as all cash returned to banks. In many interviews, one of Modi’s economic advisors, Rajeev Kumar stated that all currency which returned to RBI is not legal and enquiry of shady accounts is still on.[9] Account holders, to whom notices are served, can go legal or settle with the government, silently. Those who take the first route will do it at the cost of their social capital. An associated issue is related to the money deposited in Jan-Dhan accounts. For simplicity, assume that money returned from Jan-Dhan accounts to original owners after demonetisation. Since the origin of the money from all accounts is known after demonetisation, money trail can be traced. It is also possible that people might be waiting for the opportune moment to take their money back from Jan-Dhan account holders. In such a scenario, Jan-Dhan account holders have an incentive to bring Modi back into power in 2019.

Similar to demonetisation, the majority of the landlords were able to save their land by changing land use and land ownership. Nehru envisioned a great reform but failed to understand ground realities. Still, land reforms brought major political gains to Congress and sustained throughout Nehru’s life. Should we accuse Nehru and Congress for land reform to reap political benefits? How can anybody accuse Modi for crippling his political rivals while sparing Nehru and Congress party for reaping rich political dividends out of land reforms.

Demonetisation must also be evaluated around contemporary policy discourse. Joseph Stieglitz, ex-president of World Bank, in his work ‘Globalisation and its Discontents’ deliberates on the need of institutional change to govern globalisation. Joseph Schumpeter’s idea of creative destruction and paradigm shift in institutional order is not alien to mainstream academia. Institutional change under UPA was either ignored or delayed which created space for crony capitalism which eventually crippled the entire economy. Most of the corruption cases during UPA rule were due to failure to change rules when the nature of the economic game was changing. Demonetisation definitely was part of a disruptive shift as far as administration and governance of financial institutions in India is concerned. Demonetisation along with other legal-economic reforms e.g. Jan-Dhan accounts, bankruptcy code, direct benefit transfers, Mudra loans, various public insurance plans has made the banking sector more inclusive, more informed and more accountable than any time before in history. It was unthinkable in 2014 to identify economic offenders. At least, few new rules are now in place to fill the void and pieces of evidence suggest that change in rules of the game matter significantly. For example, London lower court verdict against Vijay Mallya is a direct effect of new rules.

It is a known fact that public sector banks in India had been facing bad debt issue before NDA came to power in 2014. Crippled public sector banks extended leverage to “private sector” banks to keep lending rates high. Demonetisation brought short term relief to public sector banks by increasing cash deposits with banks. High cash deposits in banks meant that they can lend more and can compete with private sector banks at least in the short run. It must be remembered that UPA II under Manmohan Singh used public sector banks to “bail out” “private entrepreneurs” after the financial crisis in 2008.[10] How can bailing out “public sector banks” be worse than the bailout of “private” entrepreneurs” using public money? It was common people who bled in both cases but the difference between the end beneficiaries cannot be ignored. Demonetisation was an effort to bail out people’s institution (public sector banks) instead of bailing out crony capitalists e.g. Vijay Mallya and Nirav Modi.

Vilifying demonetisation and calling it failed economics is futile. There are both good and bad sides of every policy decision and only a careful cost-benefit analysis can inform about net present benefit from demonetisation. The opposition is targeting demonetisation by questioning its opportunity cost but there is deft silent on gains to society. The economy is far from doom. Economic growth is definitely moderate; however, inflation and fiscal deficit is kept within acceptable limits. There is recent debate regarding the employment effects of demonetisation; however, both sides in this debate have their own biases. It is not rocket science to understand that a disruption like demonetisation will cause labour force adjustment. Now, claiming that there has been no adjustment is as foolish as to claim that perfect adjustment has occurred.

The opposition is in awe and fear not because they are the only corrupt people in the political system but because ‘the honest’ and ‘the reformer’ image of Shri Modi gives BJP hegemonic leverage over rest of the political parties. To counter the BJP, Rahul Gandhi is raking up Rafael issue and targeting the PM himself. At present, convergence of disgruntled allies e.g. Shiv Sena, Asom Gana Parishad etc. and many Congress leaders towards BJP before general elections hints that Congress has failed to counter BJP’s expansion in the Indian political space.

(The writer is (PhD, Economics), Research Associate, IIT Bombay)

Courtesy: Academics4Namo

[1] https://www.youtube.com/watch?v=OknuVaSW4M0

[2] https://www.mbauniverse.com/group-discussion/topic/business-economy/demonetisation

[3] https://economictimes.indiatimes.com/tdmc/your-money/demonetization-anniversary-decoding-the-effects-of-indian-currency-notes-ban/articleshow/61579118.cms

[4] http://mofapp.nic.in:8080/economicsurvey/pdf/001-031_Chapter_01_ENGLISH_Vol_01_2017-18.pdf

[5] https://en.wikipedia.org/wiki/Monetary_base

[6] http://www.economicsdiscussion.net/banks/credit-creation-by-commercial-banks-and-its-limitations/4155

[7] http://14.139.60.114:8080/jspui/bitstream/123456789/711/11/Nehru%20and%20the%20Agrarian%20Reforms.pdf

[8] http://shodhganga.inflibnet.ac.in/bitstream/10603/102421/6/06_chapter%201.pdf

[9] https://www.youtube.com/watch?v=1-Ie7uOKNN8

[10] https://www.businesstoday.in/magazine/features/the-indian-bailout/story/3398.html