Intro: India needs a better customised and well targetted farm sector loans policy for the exclusive benefit of real cultivators, including tenant cultivators.

India is the world's second largest food producer with highest number of farmers and farming-dependent population. This vast section of population has been witnessing ever growing distress with sagging confidence in farming, largely on account of inept policy interventions of the post-reforms period, especially in the last 10 years' UPA rule wherein, the agricultural loans were being diverted to industry and commerce, by deliberate and protracted dilutions in the definition of agricultural credit for the window-dressing of UPA Government’s achievements. The recent enhancement of the provision for agriculture credit to Rs 8.5 lakh crore, along with a slew of many other measures in the Union Budget for 2015-16 of the NDA Government can indeed alleviate the plight of farmers effectively, provided the access of the farmers to agricultural credit is again restored.

Deliberate Dilutions: Policy dilutions, leading to financial exclusion of poor farmers had been initiated as early as in 1993, when Dr Manmohan Singh was the Finance Minister. Till 1993, only direct finance to cultivators was counted as part of the priority sector lending, for meeting the target of 18 per cent bank credit for agriculture. But, from October 1993, indirect finance was also allowed to be counted together with the direct finance to cultivators for fulfilling the priority sector target of 18 per cent loans for agriculture. The government has thereafter, kept on diluting the definition of 'indirect credit to agriculture' to include even the corporate borrowings as well as infrastructure project fundings in indirect agriculture credit. By virtue of this, even the loans given to the multinational companies like ITC and other contract farming and agri-processing companies too are now being counted into the quantum of loan extended to farmers, which amounts to almost up to 50 per cent of farm sector indirect loans in states like West Bengal etc. Only four of such one dozen dilutions made by the government are enough to be given hereunder to expose the tactical deprivation of real farmers from agriculture credit under the decade long regime of UPA. These dilutions are:

- (i) The loans given to even power distribution companies, emerging out of the bifurcation or restructuring of SEBs as part of power sector reforms were ordered to be considered as indirect finance to agriculture from July 2005.

- (ii) The loans to food and agro-based processing units with investments in plant and machinery up to Rs 10 crore (other than the units run by individual, Self Help Groups and cooperatives in rural areas) are also being considered as indirect finance to agriculture since April 2007.

- (iii) From April 2007 onwards, two-thirds of loans given to corporates, partnership firms and institutions for agricultural and allied activities (such as beekeeping, piggery, poultry, fishery and dairy) in excess of Rs 1 crore in aggregate per borrower have been declared to be considered as indirect finance to agriculture.

- (iv) From October 2012, the loans given to corporates, partnership firms and institutions for agricultural and allied activities in excess of Rs 2 crore in aggregate per borrower are also defined to be treated as indirect finance. Even such loans of amount less than Rs 2 crore are being treated as direct finance.

Indeed, the indirect loans which were less than 15 per cent in 1980s have now crossed over to 25 per cent of total agri-credits, which are never accessed by the farmers.

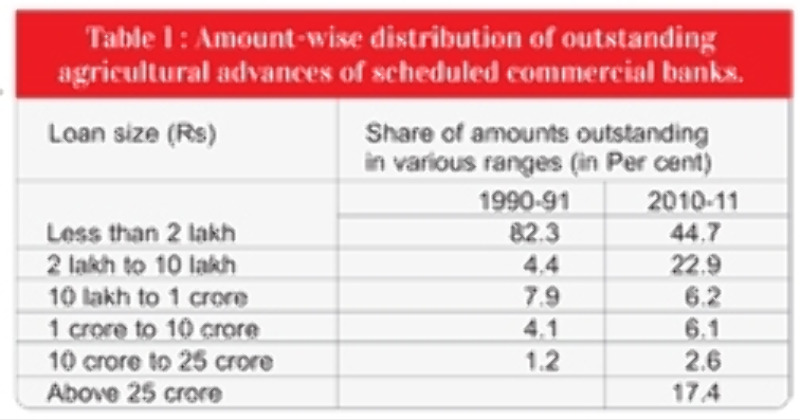

Growing Dominance and Non-Cultivating Borrowers: Since 2000, the advances of Rs 10 crore and above, and even up to Rs 25 crore are on increase while no ordinary farmer can afford to borrow such huge sums. Table 1 clearly shows that the share in total of advances of the loans of size “less than Rs 2 lakh” have contracted from 82.3 per cent in 1990-91 to 44.7 per cent in 2010-11. On the other hand, the share in total advances above Rs 10 crore increased sharply from 1.2 per cent in 1990-91 to 20 per cent in the year 2010-11. Farmers normally cannot take a loan of Rs 10 lakh or more. Mostly the cultivators do not take a loan of more than Rs 2 lakh. So, probably the increasing share of agri-credit must be going to the input dealers or agri-business firms or corporate groups involved in agricultural and allied activities.

Urban Centric Loans on Rise: The real farmer is mostly village dweller, while, there is an increased absorption of agricultural credit from urban and metropolitan branches, depicting a fall in the share of agricultural credit in rural areas. In 2011, (Table 2) about one-third of total agricultural credit and one-fourth of direct agricultural credit were outstanding from bank branches located in the urban or metropolitan areas reflecting continuing diversion of agricultural (indirect) credit towards urban-based dealers and agricultural (direct) credit to urban-based corporates (as part of direct credit) and altogether depriving the real farmers based in rural areas.

Uneven Disbursement across the Year: It is most astonishing that over 40-45 per cent of annual agriculture loans are often disbursed in the last quarter of the financial year by most of the commercial banks, probably just to meet their targets. Of this fraction also about one third to half of it is often disbursed in the last month of Financial Year (FY) i.e. March itself. The last quarter of a financial year or the month of March is not the normal period of borrowing by the farmers when the sowing is over.

Growing Dependence on Non-Institutional Lenders: Continuous deprivation of real farmers from institutional credit has been compelling them to depend more upon the exploitative and non-institutional lenders. Therefore in the All India Debt and Investment Survey of the National Sample Survey Organisation in the 70th round reveals that non-institutional agencies played a major role in advancing credit to the households, particularly in rural India. The non-institutional agencies had advanced credit to 19 per cent of rural households, while the institutional agencies had advanced credit to 17 per cent households.

Prohibitive Pre-Sanction Costs: Since, almost 50 per cent of the farmer are small and marginal farmers and the agriculture loans are not cost free and the farmer approaching a bank for a loan of over Rs 1 lakh, has to spend more than 3,000 just for documentation. This expenditure of 3 per cent of the loan value even before the loan is disbursed is a prohibitive levy.

Plight of Farmers: In 2013-14 as well as 2014-15 the unseasonal heavy rains, thunder and hailstorms have ravaged the due-for-harvesting chana, lentils and wheat in Madhya Pradesh, wheat mustard, cumin and all other crops in Rajasthan and onions and grapes in Maharashtra. Instead of an expected bumper harvest on the back of excellent monsoons, farmers reaped only misery.

To conclude, India needs a better customised and well targetted farm sector loans policy for the exclusive benefit of real cultivators, including tenant cultivators. Indirect agricultural loans are altogether being stopped from being reported as agriculture loans, atleast to arrive at the priority sector lending targets. In addition to it the insurance outreach for farm sector too needs to be spread fast, as hardly 5-10 per cent of the farmers are able to avail crop insurance benefits. Plight of the ordinary farmers can be well understood from the mere fact that if 3 lakh farmers have committed suicides since 1991 in the country, the remaining 100 million farmers and their families too are surviving in the same socio-economic circumstances, in which those 3 lakh have committed sucide. Hence, agriculture needs a 360 degree approach for the redressal of their problems to alleviate the plight of Manmohanomic reforms.

Dr Bhagwati Prakash Sharma (The writer is a Vice-Chancellor of the Pacific Academy Higher Education and Research, Udaipur, Rajasthan)