Dr Ashwani Mahajan

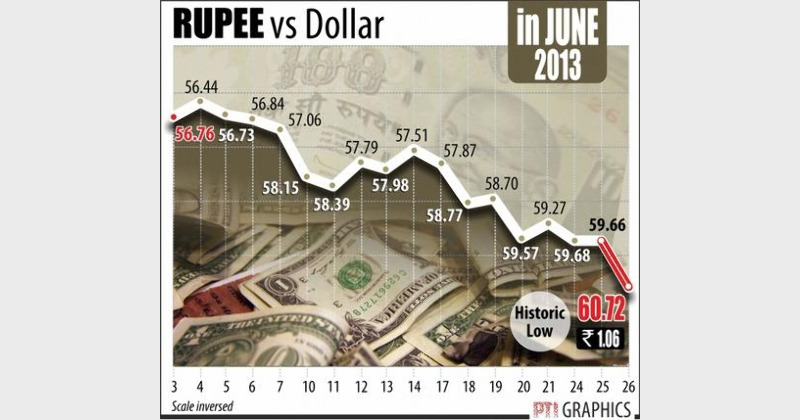

Rupee has declined by rupees 6 per US $ in 60 days, and has sunk to Rs. 60 per US$ from Rs. 54. Finance Minister says there is no reason for panic as the government is taking steps to push growth. Chief Economic advisor, Raghu Rajan says that it is not unique to India, as dollar is getting stronger vis-a-vis Asian currencies. Though some currencies are getting weaker, decline of rupee cannot be attributed to the strength of dollar.

On the outset, notwithstanding the statements for the official quarters, few conclusions can easily be drawn about the present scenario.

Firstly, the situation is very grim, as rupee has depreciated by at least 12 per cent in a short span of time. In the last five years rupee has depreciated from nearly Rs. 40 per US $ to Rs. 60 per US $. This is not only making the life difficult for the commoners, but is also causing deepening of payment crisis. Depreciation of rupee reduces the credibility of the country internationally.

Secondly, such a drastic depreciation cannot be justified on the grounds that it may help our exports to grow or it may benefit the exporters, as this is the usual argument in favour of depreciation of the currency. In fact the nation enjoyed the best of balance of payment positions in the times of strong rupee. For instance between 2001-02 and 2007-08, when rupee was going strong, in the first three years nation had surplus in balance of payment and in the next three years, deficit in the balance of payment remained less than 2 per cent of Gross Domestic Product (GDP).

Thirdly, weak currency causes nervousness amongst the people and depresses the mood of the nation, as it relates to weakening economic position. Revision of petrol prices twice within a fortnight have sent negative signal, and indicates at further fuelling of inflation. It is generally accepted fact that inflationary spiral has been depressing our growth process; as GDP growth decelerates to nearly 4.9 per cent during 2012-13, from nearly 8 per cent three years ago. This weakening of rupee is doubly bad, as it is taking place in otherwise depressing situation in the form of weak sentiments in terms of industrial growth rate and general GDP growth rate.

Why rupee is sinking?

Actually, fast increasing Current Account Deficit (CAD) in Balance of Payment and the resulting foreign exchange crisis, is the main cause for this situation. CAD is rising because of huge and constantly rising Balance of Trade (BoT), due to fat and fast rising import bill and lagging exports. For the last so many years, the government has been a mute spectator to the fast rising imports. Though petroleum products traditionally have been major item of our import bill comprising nearly one third of our imports, precious metals like gold and silver never used to be of great importance earlier. Likewise, telecom, project goods like power plants etc. never used to carry much importance in our imports, a decade back. However, in the recent years their share has gone up. Import bill of gold and silver has increased from $22.8 billion in 2007-08 to $61.3 billion in 2011-12. Recent spurt in imports of these items has been the major cause of increase in our import bill. In the last three years our trade balance from China has gone up to $40 billion in 2011-12, from nearly $27 billion in 2007-08. It is not out of place to mention that on March 31, 2008 exchange rate of rupee was Rs. 40 per US$ which increased to Rs. 51.2 per US$ by March 2012 and now in June 2013 it is Rs. 60 per US$. Major reason for spurt in imports from China is increase in telecom and power plant equipments, project goods and continued imports of electronic and electric goods. Trade balance with rest of the world is also rising fast. Amidst this scenario of sinking rupee, the government is finding itself completely helpless. Government and The Reserve Bank of India (RBI) both fear that any intervention to stem fall of rupee may deplete of foreign exchange reserves.

According to RBI Bulletin, June 10, 2013, our trade balance has crossed US$ 191 billion and CAD is also expected to be near $100 billion. It is notable that in this era of globalisation, our imports have been rising at record pace and import bill increased in leaps and bounds, from $24 billion in 1990-91 to $492 billion in 2012-13. In terms of per cent, the GDP imports were hardly 8.1 per cent of GDP, which went up to 28.3 per cent in 2012-13. Exports also did increase during this period, but only to 17.3 per cent from 6.1 per cent of GDP. As a result our trade balance increased from merely 2 per cent to 11 per cent during 1990-91 and 2012-13.

Surplus in BoP during NDA Regime

Between 2001-02 and 2003-04 National Democratic Alliance (NDA) regime, it so happened that our Balance of Payment (BoP) deficit turned into surplus, continuously for three years. However, after 2004, our CAD did not stop rising and by 2012-13, it has crossed all limits. Between 1990-91 and 2000-01, our average CAD was only $4.4 billion annually. However, in 9 years, between 2004-05 and 2012-13, CAD has reached $37.4 billion (which is 8.5 times of average CAD in 1990s). Whereas, total balance of trade deficit in ten years between 1990-91 and 2000-01 was $103.56 billion, between 2004-05 and 2012-13, the same were $988 billion. Huge remittances from NRIs and great earnings from software exports, even during the most difficult years of global economic crisis also proved to be insufficient to make good this deficit.

Government is disillusioned even today

Today, the sole remedy being suggested and applied is encouragement to foreign investment, both Foreigh Direct Investment (FDI) and portfolio investment. It is notable that the government has been giving red carpet welcome to foreign investment, and now expecting that the foreign investment can suddenly be increased out of proportion, and the nation can solve the problem of payment crisis in a short period of time, does not seem to be practical. Therefore, only possibility left with the government is to raise more commercial loan, which has already been hinted at by the Finance Minister. But this remedy would be worse than the decease itself. Increase in external debt again involves repayment of interest and principal in future. Compulsion to raise external commercial borrowings may also further reduce our credit rating. It is notable that total outgo on repayment of interest and principal in 2011-12 was $31.5 billion. Foreign investors were also not behind in remitting funds abroad in the name of interests, dividends, royalties, salaries etc., and sent $26 billion in 2011-12. Studies reveal that much larger amount of foreign exchange is remitted abroad illegally by foreign companies by way of transfer pricing and circumvention of law of the land. Under these circumstances, we find that the nation is heading towards a deep foreign exchange crisis. For a long time, all our efforts to increase exports are not fructifying, while imports are increasing by leaps and bounds. Today it is imperative for the government to impose effective restriction on imports, especially of consumer goods, telecom, power plants and other project goods, capabilities of producing of which exist in India. Effective curbs on imports of gold and silver, provision of lock-in-period on FIIs could also help. Blind policy of encouraging FDI and FII may prove to be disastrous for the nation in the long-run. Rather, it is also imperative to restrict foreign companies to take away foreign exchange illegally, by way of transfer pricing and/or circumventing law of the land. Failure on the part of the government to take effective and timely steps may push the nation to deep payment crisis.

(The writer is Associate Professor, PGDAV College, University of Delhi and can be contacted at Email: [email protected])